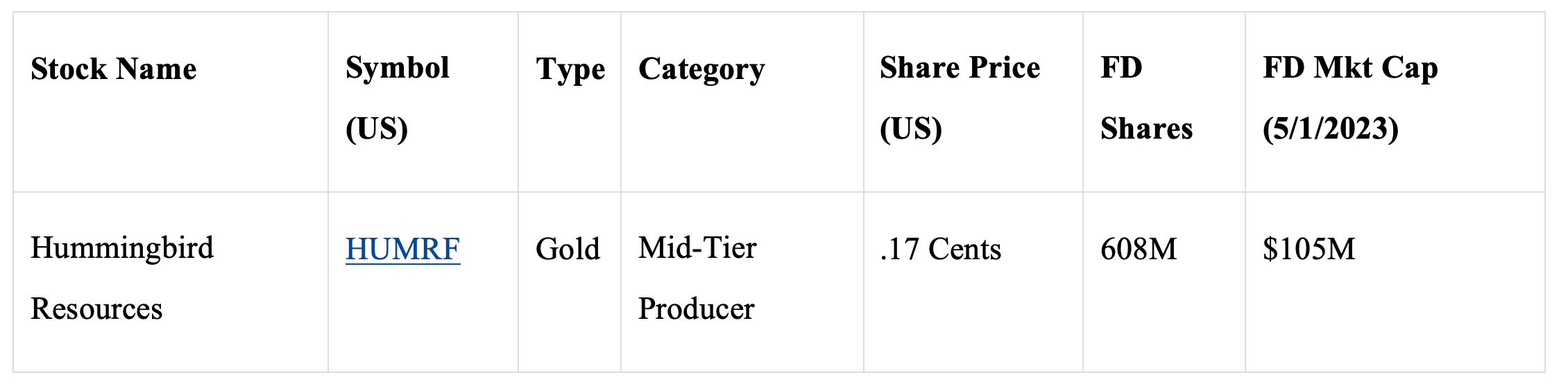

Hummingbird Resources: Mid-Tier Gold Producer.

Hummingbird Resources: Mid-Tier Gold Producer.

May 4th 2023

Summary

They are finally turning things around and heading in a good direction.

They have a second operating mine scheduled to come-online this quarter, Q2 2023, expect to double the company’s production profile.

They are not for sale as an acquisition target, with strong insiders who want to see this company grow into a large mid-tier producer.

They are highly leveraged for higher gold prices, with the potential for high free cash flow.

Introduction

Back in 2008-2009, I learned something that was useful. If you can find a mid-tier producer that has been beaten up by investors and is selling for about half its value, plus is poised to add production, the risk-reward can be tremendous.

Hummingbird Resources fits those criteria. Its currently forecasting 80,000 to 90,000 oz production this year from their current operating mine, Yanfolila in Mali, with a valuation of only $105 million and is expected to increase production to 200,000 oz (annual rate) in the next few months as its second operating mine in Guinea, Kouroussa comes on line.

There are some reasons for its low valuation. First, its mines are in West Africa (Mali, Guinea, and Liberia), which are not always viewed positively by investors. Second, its costs have not been that low historically (but are improving materially, as seen by their last two quarters). Third, it has been a poor share price performer the last few years, mainly driven by poor operational performance from Yanfolila. Fourth, they currently have around $120M in debt. Fifth, they are based in London and currently only trade on the OTC Pinks in North America. However, they are reviewing their North American listing and may support OTCQB soon.

But don’t stop reading yet. There is a lot of offsetting good news.

Company Overview

Yanofolia (Mali) has a Resource base of 2.1M oz (2.2 gpt), is an open pit operation currently, with an underground mine being developed, scheduled to be into production by year-end, for a full year of production from the underground in FY2024. They are forecasting at Yafolila for FY23 production of 80,000 – 90,000 oz at an AISC of <$1,500 per oz. Last Qtr, they produced 27K oz with an ASIC of $1,109, so Yanfolila guidance for FY23 should prove conservative in my view.

Their second mine is Kouroussa in Guinea. It has a high-grade 1.2M oz open pit Resource (3 gpt, and 4 gpt for their Reserves), with underground potential. The company just announced that commissioning at Kouroussa has commenced, with first gold pour expected this quarter (Q2 2023), with updated FY23 guidance to be given once Kouroussa is ramping up.

After the Kouroussa ramp-up, the company expects to be a 200,000+ oz gold producer. The mine remains on time and on budget ($115M capex). They have begun the commissioning phase toward first gold pour. It was financed from Coris Bank International, internal cash flows, and a raise of $17M that was completed in February.

They now have a clear, near-term path to increase production to 200,000 oz of production run rate in 2H 2023. Between Yanofolila and Kouroussa, they shouldn't have a problem making their debt payments of about $25M per year.

Their third project is Dugbe (Liberia). It is an advanced (feasibility study completed June 2022) 4M oz (1.5 gpt) open pit project. It is a large capex project, which won’t be easy to finance. They have a joint venture agreement with Pasofino Gold (listed on the TSX), who completed the feasibility study in June 2022 to earn-in 49% of the project, with Hummingbird retaining a 51% majority ownership.

Pasofino also has an option to obtain 100% of Dugbe, with Hummingbird’s 51% majority stake replaced with a 51% majority stake in Pasofino’s shares. Currently, there is a strategic review underway by Hummingbird and Pasofino on the best ways to realize the maximum value of Dugbe.

Dugbe has a $690M NPV at $1,700 gold. One way or another, Hummingbird will eventually get some value from Dugbe, but currently, it is getting zero value. I like the fact that they have strong insiders and have no plans to sell. Plus, they have a goal of growing the company to be a 350,000 to 500,000 oz producer in the years to come.

If they succeed at reaching 350,000 oz of annual production and gold trends above $2,500, they could easily have huge returns. Also, with their new, high-grade mine Kouroussa set to come online this quarter, taking them to a 200,000+ oz producer, risk-reward is clearly to the upside not yet valued in the stock. The risk-reward looks very appealing at this time. Yes, it has risk, but it also has the potential for very high returns.

They are currently trading at about 2.5x FCF (free cash flow). However, they are adding FCF soon at Kouroussa. So, they will be trading at less than 2x FCF if their valuation does not increase. Management is planning to do more marketing to investors this year to recognize that value.

It should also be noted that they consider themselves shareholder friendly. One proof of this statement is that they do not have a lot of cash on their balance sheet and don’t have any plans to do further financing this year.

Most companies with a low cash position would do a financing prior to ramping up production at a new mine to reduce their risk exposure in case something goes wrong. I consider it a positive that they are confident they don’t need it. This shows me that they realize a financing will only harm shareholders at this time.

Company Info

Cash: $8M

Debt: $120M

Current Gold Resources: 7.3M oz (Company Reserves 4.13M oz).

Estimated Future Gold Resources: 7.3M oz.

Estimated Future Gold Production: 200,000 oz.

Estimated Future Gold All-in Costs (breakeven): $1,100 – 1,200 per oz

Scorecard (1 to 10)

Properties/Projects: 7

Costs/Grade/Economics: 7

People/Management: 7

Cash/Debt: 6

Location Risk: 6.5

Risk-Reward: 7.5

Upside Potential: 9

Production Growth Potential/Exploration: 7

Overall Rating: 7.5

Strengths/Positives

Significant upside potential

Near-term production growth

Good grade

Good management

Quality properties

Risks/Red Flags

High debt/weak balance sheet

High costs historically

Management has not been a stellar performer and still needs to prove itself

Location risk in West Africa

Future Upside Potential ($2,500 gold prices)

Gold production estimate for the long term: 200,000 oz.

Gold All-In Costs (break-even): $1,100 -$1,200 per oz.

200,000 oz. x ($2,500 - $1,600) = $180M annual FCF (free cash flow).

$180M x 8 (multiplier) = $1.4B

Current FD market cap: $105M

Upside potential: 1,200%

Note: I used a $2,500 gold price because I am a long-term investor who plans to wait for higher gold prices.

Note: My All-In Costs are the expected costs that will generate FCF (free cash flow).

Note: I used a future FCF multiplier of 8 because I’m confident that investors will bid up its valuation when they have large margins and pay off their debt.

Balance Sheet

Hummingbird has about $8M in cash and $120M in debt (with further debt facilities available if needed). They are generating around $40M a year in FCF at $1,990 gold. Plus, they will increase their FCF materially once Kouroussa comes online this quarter, Q2 2023. Their current balance sheet is a risk; however, it should be less of a risk once Kouroussa ramps up into production. I am not risk-averse and have no problem assuming this added risk, but I'm highlighting it for you.

Their $120M debt has an aggressive payback schedule of $25M per year for the next four years. This is both good and bad. If they can make those payments, then their balance sheet will clean up rapidly. However, if they have trouble, that could lead to higher share dilution or possibly bankruptcy.

Risk/Reward

The main risks in my view, are their debt levels and the location of their mines, which are in higher risk countries.

In the long term, there is the potential for higher taxes and royalties, which can reduce the expected upside. Inflation or other factors can push up costs, and a myriad of things can go wrong. So, this is not a slam dunk, although I think the risk-reward is compelling.

To take on this high risk, the reward has to be high. For Hummingbird, I think outsized returns are likely if the price of gold trends higher. Anything above $2,200 and Hummingbird should take off higher. But what I really want are gold prices at $2,500 or higher, for big returns.

Investment Thesis

I want to be overweight gold producers and own as many high-quality mid-producers as possible (as long as I can find them cheap). Moreover, I like to find undervalued producers that are likely 5-baggers at $2,500 gold and potential 10-baggers at even higher gold prices. Hummingbird fits this strategy.

I don’t know which gold miners will perform the best, so I use a low cost-basis allocation strategy to lower my risk for individual companies. Instead of using concentrated positions, I prefer to allocate 1% or less per stock. For higher-risk stocks such as Hummingbird, I will only allocate around .5% (less than 1%). This takes the emotion out of it and reduces the need to trade if they drop in value. As a result of this strategy, I tend to own a lot of stocks.

I realize that Hummingbird has risks, and this is why I keep my allocation low. I also realize that to reach my objective (high returns), I will have to be patient and wait for higher PM prices (this could take several years). So, this is a buy-and-hold stock. I consider it another high-upside stock added to my portfolio. If gold does reach $3,000, I can see which ones performed the best. My bet is that Hummingbird will have done better than many expected.

What's your view on the open offer?