GSD October Newsletter

Free to the public for marketing purposes. First time ever!

Previous Month ( )

AU: $1663 ($1737)

AG: $18.86 ($18.78)

HUI: 191 (195)

DXY: 111 (108)

S&P: 3640 -24% (4030 -16%)

10-Yr: 3.7% (3.1%)

Oil: $81 ($97)

Let’s begin by looking at the numbers above. The stock market was down in September. We have one more day, but the S&P is now down 24%, which is a correction low. I still expect a low between 3000 and 3300, which is another 10% to 20% lower.

Gold was down $74 for the month, but the HUI has been somewhat resilient, as investors expect gold to rebound. Silver was actually up for the month, signaling that it is primed to rally. I think the silver bottom might be in, although I expect gold to go lower, and potentially could drop to $1550 if the S&P hits 3000. Gold traded at $1615 in September, which potentially could hold.

The DXY went nuts in September, almost touching 115. However, it appears to have topped out after rolling over yesterday back to 112. It could make another resurgence, but I think it is clear that we are not going to see 120 because the market wants to price in a Fed pivot. Note that this reversal in the dollar is good for gold and silver. The surging dollar has been a headwind that gold and silver could not withstand.

Interest rates also went nuts in September, with the 10-year US Treasury Bond reaching 4% (currently back to 3.7%). Below are the current interest rates. The 1-year is at 4% and the 30-year at 3.65%. Thus, it is inverted, signaling a looming recession.

The macro picture remains bleak for the economy. The 30-year mortgage rate is over 6%, which is killing housing. Inflation remains at elevated levels, creating headwinds for consumer spending, which is 70% of the economy. The big four household budget items of rent, food, utilities, and transportation are all facing inflation pressures. Consumers are getting squeezed, and they don’t have much left over to spend on other items.

I think mass layoffs are coming soon as lower consumer spending creates a drag on corporate earnings. Once that happens, the recession will begin to bite. Unfortunately, this will create a negative feedback loop, whereby layoffs will only make matters worse for the economy. So, the real pain is ahead.

My last two newsletters had a similar tone. Now it is becoming apparent that I am likely right. What could possibly happen to prevent this outcome? Inflation begins to wane, and the Fed to implements QE to reignite the economy? I doubt it.

Instead of the economy coming back to life, a situation is unfolding that will likely ignite a fear trade into gold. I think this is very similar to 2008. From March 2008 until October 2008, the GDX was down 71% (56 to 16). It was an 8-month correction. After gold and the GDX bottomed in October 2008, they went on a 3-year bull market rally. That rally saw the GDX go from 16 to 66, a 300% return. That was for large-cap miners.

I think the same thing that happened in 2008 for gold and the GDX is playing out again. Ironically, the current correction also began in March. We are now entering the 8th month of the correction. The GDX is only down 50% (42 to 21), although it could go lower before this correction ends. I expect the returns to be even better than from 2008 to 2011, as gold potentially flies to $3,000 or higher.

We still need to get above important resistance levels of $2050 gold and $30 silver, but I expect that outcome in 2023. The technical charts for both gold and silver are strongly set up for a breakout. Both are in a massive cup and handle formation. Once gold gets above $1900, it will be hard to stop it from running to an ATH. Once silver gets above $27, it will be hard to stop it from getting above $30, which sets up a likely quick run to $35 and beyond.

Here are the monthly gold and silver charts.

Okay, we know what is happening with the economy. September made that obvious. The economy is slowing. The question now is how fast does it slow and how much. Do we get a financial crisis? Do we get a plethora of mass layoffs? One thing that seems certain to me, the Fed will raise at least one more time in early November. After that, they could perhaps raise once more, but a pause is coming. That is inevitable.

Will the coming pause be enough to restart the economy and the stock market? I doubt it. So, the Fed is betting that the economy and stock market do not crash while they pause. This means that the economy is likely to muddle over the next 6-12 months. This also means the stock market will not have the Fed put they so desperately need to trend higher. Wall St believes the Fed will not allow the economy to crash and will begin QE (money printing) and lower rates in 2023. That is really the only outcome that could prevent a gold breakout. But is it likely?

After September, it has become obvious that systemic risk is becoming more noticeable. The BOE (Bank of England) had a crisis this week as the GBP (British pound) crashed versus the dollar. That is not likely to be the last crisis in the near term. The one thing I have reiterated over and over in this newsletter is that the only reason to own gold is to protect against systemic risk (or to bet on that outcome). Well, we are likely entering a period of high systemic risk. If this is true, then gold should begin to trend soon.

Here is my favorite gold chart, which is Exter’s Pyramid. The big-money players only run to gold when their other assets become too risky to hold. In other words, they only buy gold when systemic risk is pervasive. That time could be now.

It is my opinion, that the US era of dominance is coming to an end, and this is the decade of transition. If I’m right, then a new global financial system will be needed, whereby the dollar is steadily decreased in global trade. Once this transition begins, I would expect the dollar to begin to fall and gold to begin to rise, due to uncertainty. When you count the number of dollars in circulation both in the US and globally, along with the amount of debt denominated in dollars, it is a massive number into the multi-trillions. Only a tiny percentage of that needs to move to gold for it to explode upward.

While this transition will not begin in the near term, the precursors likely will. What are those precursors? A recognition that the US economy is weakening to the point that US govt bonds (US Treasuries) are no longer AAA rated. A recognition that the US is flooding the world with inflated dollars (our trillion-dollar budget deficits) and abusing its privilege of being the world reserve currency.

About 79% of Global trade is currently transacted using US dollars. This is likely to begin shrinking as a result of the Ukraine invasion. Once this begins shrinking, it is going to put pressure on both the dollar and US interest rates, as demand for dollars declines.

The BRICS+ make up about 50% of the global population. I expect them to release a new currency in 2023. My guess is that this is currently under discussion and near finalization. The two countries behind this are China and Russia. This will be a game-changer for international trade and bad for the US economy and the US dollar. It will also likely increase systemic risk to the global financial system, considering how much debt is denominated in dollars.

Winter begins in October for most northern climate countries, such as Europe. There have been no recent peace negotiations in Ukraine, so we can expect this war to rage all winter. The Nordstream 1 & 2 natgas pipelines have been sabotaged and are not likely to be used this winter in Europe. This means natgas shortages in Europe. How will this impact Europe’s economy? I think a recession is to be expected, putting more pressure on the global financial system.

Most large US corporations get about half of their revenue from global sales, and Europe is one of their largest customers. This means many of them are likely to do mass layoffs once a recession in Europe begins.

Perhaps I’m wrong and systemic risk will be contained, and the big-money players will be content to hold US Treasuries and dollars instead of gold. That’s a possibility, but the world is probably heading into a deeper crisis today than in 2008. We are going to find out over the next few months if this is indeed true, and perhaps as soon as October. The world hasn’t been this destabilized since WW II. This is worse than 2008. At least, that’s my take.

If I’m right, then systemic risk will be on the rise in Q4 and into Q1. If the world does not reverse the economic trend that it is currently on, then gold should be much higher over the next few months as the fear trade into gold takes hold.

To close, many of you are always interested in my targets for gold and silver in the near term. It’s impossible to call a bottom in advance, but I think we are getting close. Gold might have bottomed in September at $1615, although I think we could see $1550. Silver has had good PA (price action) the last few days and is acting like the bottom is in, which was $17.50 in September. The HUI has also had good PA of late, and it might have also put in a bottom at 172 in September. I think we will know the bottoms of all three by the end of October.

Stocks in the News

Beaver Creek Gold & Silver Mining Conference

I met with about 50 gold & silver mining companies doing one-on-one interviews as a guest of Lawrence Lepard. I learned quite a bit, but mostly that my analysis was mostly accurate. I did become more bullish on some stocks and less bullish on others, but overall, I came away convinced that I know how to analyze PM mining stocks.

Here are some of my takeaways:

K92: Their project is a monster that just keeps growing in size. And their low costs make it attractive. The CEO is excellent.

Westgold: It looks really solid. I was impressed by their team, strategy, and projects.

Osisko Mining: Not great upside, but a great mgt team. I expect them to be a growth story.

Americas G&S: The upside looks big. Mgt has not executed well, but they have the properties to be a rocket ship at higher gold/silver prices.

Chesapeake: They have figured out their heap leach sulfphide method. But it is going to take a long, long time for them to ramp up production. It's an excellent

optionality play for the long term.

Lion One: They are finding high-grade gold at depth. I think this could be a large mine. They announced a 400 gram meter hole this week. I expect more of these.

Montage: They have 5 million oz, and this total is going to grow substantially. It's cheap, and a good optionality play.

Revival: They have a 4 million oz project in Idaho. Looks like construction in 2024. I like the CEO and expect him to build this mine.

Sabina: Another CEO that I like. They have 9 million oz at 6 gpt, plus they will find more. They will begin production in Q1 2025 at 450K oz a year.

Aya Gold & Silver: Mid-tier producer in Morocco. Expanding production at Zgounder to 8 million oz AGEQ in 2024, then to 10 million oz AGEQ in 2025. Plus, they have a new discovery (Boumadine) that could be as large as Zgounder.

Discovery Silver: Large silver development project (Cordero) in Mexico with 1 billion oz AGEQ. A production target of 30M oz AGEQ for the first 10 years. This is likely to increase before reaching year 10. PFS due in 2022. Feasibility due in 2023. Construction in 2024. Production in 2026.

Guanajuato Silver: Recently acquired 3 producing properties from Great Panther in Guanajuato near their producing El Cubo mine. Ramping up production to 6 million oz AGEQ in 2023.

Westgold Resources: Australian mid-tier producer. They look cheap. Currently a 4 FCF multiple. 265K producer at $1500 break-even. Costs should drop in 2023. Production will trend up to 300K. $150 million in cash and no debt.

Erdene Resource Development: Mongolia development project. $100 capex to produce 100K oz a year. Should get financing soon to begin production in mid-2023. $1350 break-even costs. Targeting 2M oz resource in the near term. A lot of drill targets.

Ascot Resources: British Columbia development project. Trying to borrow $100 to $125M USD, + $15M Equity to finance the Capex. 150K year production. Growing to 170K year production. $1300 break-even costs. They are confident they can finance the Capex. If so, then construction in 2023.

Cassiar Gold: Large property (150,000 acres) with a lot of drill targets in Northern British Columbia. Their Taurus deposit is 1.4 million oz (1.1 g/t) and likely to double in size. Plus, they have high grade discoveries. It’s a pretty juicy drill story/development story.

Silver Tiger Metals: I was surprised by the potential of this stock. This one is going to be a large high-grade silver mine in Mexico. They have discovered an unusual formation of shale that seems to be loaded with high-grade silver. Many of the intercepts are over 1,000 gpt AGEQ.

Adriatic Metals: Their Rupice project in Bosnia looks really solid. It’s under construction, with production scheduled for Q2 2023. Production will be 15 million oz of AGEQ, with break-even costs of around $13 per oz. They have a 20-mile trend to explore to extend the mine life.

Equinox Gold: They have six producing mines (all in the Americas), and four of them have significant exploration potential. They are producing 650,000 oz and that will expand to 1 million oz in the next few years. It’s not usual to find a growth story like this one so undervalued. They are a mid-tier today, but they are destined to be worth $5 to $10 billion at higher gold prices.

I-80 Gold: They are a twin of Equinox Gold (although smaller) with about six very solid properties, all of which are in Nevada. They will expand production to 500,000 oz in the next few years. I Iiked their properties even more than Equinox, although it’s impossible to know which company will have better exploration success. So, own both. It’s crazy that these two quality gold producers are so cheap.

GoGold Resources: You should be aware of this story. They have been releasing a plethora of good drill results at Los Ricos in Mexico. The Los Ricos South PEA calls for 8 million oz of annual AGEQ production. The PFS, which is coming out soon and will be higher, at around 10 million. Phase two will be Los Ricos North, which is twice as big, and will produce around 20 million oz of AGEQ. Combined, that is 30 million oz of annual AGEQ production. Phase one production will be in Q1 2025.

US Gold: They are building the CK project in Wyoming. Many will pass on this project because the capex is high at $250 million, and it won’t be permitted until 18 months at the earliest. But this is a low cost gold mine, with break-even costs of around $1000. It has sold off and is cheap. They have a very good team and I’m confident it will get financed and built. Plus, they won’t sell early. They want a big return. Plus, they have an excellent second project (Keystone) in Nevada that we get for free. It’s 20 square miles and has only had 35 drill holes. They plan to drill it after CK is in production.

Treasury Metals: This is another one many will pass on, but if you don’t mind speculating, it looks juicy. Yes, they have had trouble advancing the project, but the CEO has assembled, and very good team and I think it is headed to production. The Goldlund/Goliath project has 3 million oz in an excellent location in Ontario, Canada. The capex is high at $275M, and permits are not expected until 2024, so those are the red flags. But they expect their resource to at least double and to likely triple. That seems optimistic, but if they double them to 6 million oz, this could fly. They have lots of drill targets on 75,000 acres. Note that a PFS is due in 2023.

Eloro Resources: This is really a potential tin mine in Bolivia, but it also has 25% revenue from silver. If silver triples in value, then the silver portion could rise to perhaps 40% or higher in revenue portion. Amazingly, they think the Santa Barbara deposit is 1400 x 500 x 600 and fully mineralized at 4 opt AGEQ. That would be 3 billion oz of AGEQ. I don’t think it is that big because that is huge. Plus, it is open in all directions. They won’t release a maiden resource until Q4 2024, so we will have a long wait to find out the size of Santa Barbara. But if it is 25% of that size, it’s still huge.

Cabral Gold: They have an excellent project in Brazil. They want to build it in two phases. Phase one will mine the oxides using a heap leach using a low $16M Capex. They will begin production at around 25K ounces in 2024 and ramp up to perhaps double that. They have 300,000 oz of oxides and expect that to double in size. This will allow them to generate FCF and build the larger hard rock mill for the sulphides. Phase two will mine 100K to 150K per year. They have excellent exploration potential, and I expect them to mine 150K per year. But that won’t happen until around 2027.

Bear Creek Mining: Most will ignore this stock because their large Corani silver project in Peru has not been financed. However, they have fixed the Mercedes mine in Mexico that they recently acquired. In Q4, they will have ramped up production to 70K oz with around $1200 to $1300 break-even costs. They will generate around $25M in FCF in 2023. This will put them on the road to eventually being able to finance Corani. In fact, I think once silver gets above $30, they will get the loan for Corani.

Troilus Gold: They are building a large 9 million oz (.8 gpt) project in Quebec. They want to build a 35K tp/d mine that produces 240K oz for 27 years. The break-even cost per oz will be around $1200. Permitting is due in 2024. A PFS is coming out soon. A feasibility is planned for 2023. The bad news is the capex is $680M. Can they finance that big amount? I think they can. Also, their property size is 350,000 acres, with exploration potential. I like this one as an optionality play.

Member Emails / Questions

Do you have a link to your Substack files?

Thanks,

Joe

My Reply:

I created a substack to make it easy to distribute ranking lists. You can subscribe using your email. It’s free. Here are the links:

Exploration Stocks #1:

Exploration Stocks #2:

Development Stocks #1:

Development Stocks #2:

Producers #1:

Producers #2:

All Silver Stocks Ranked:

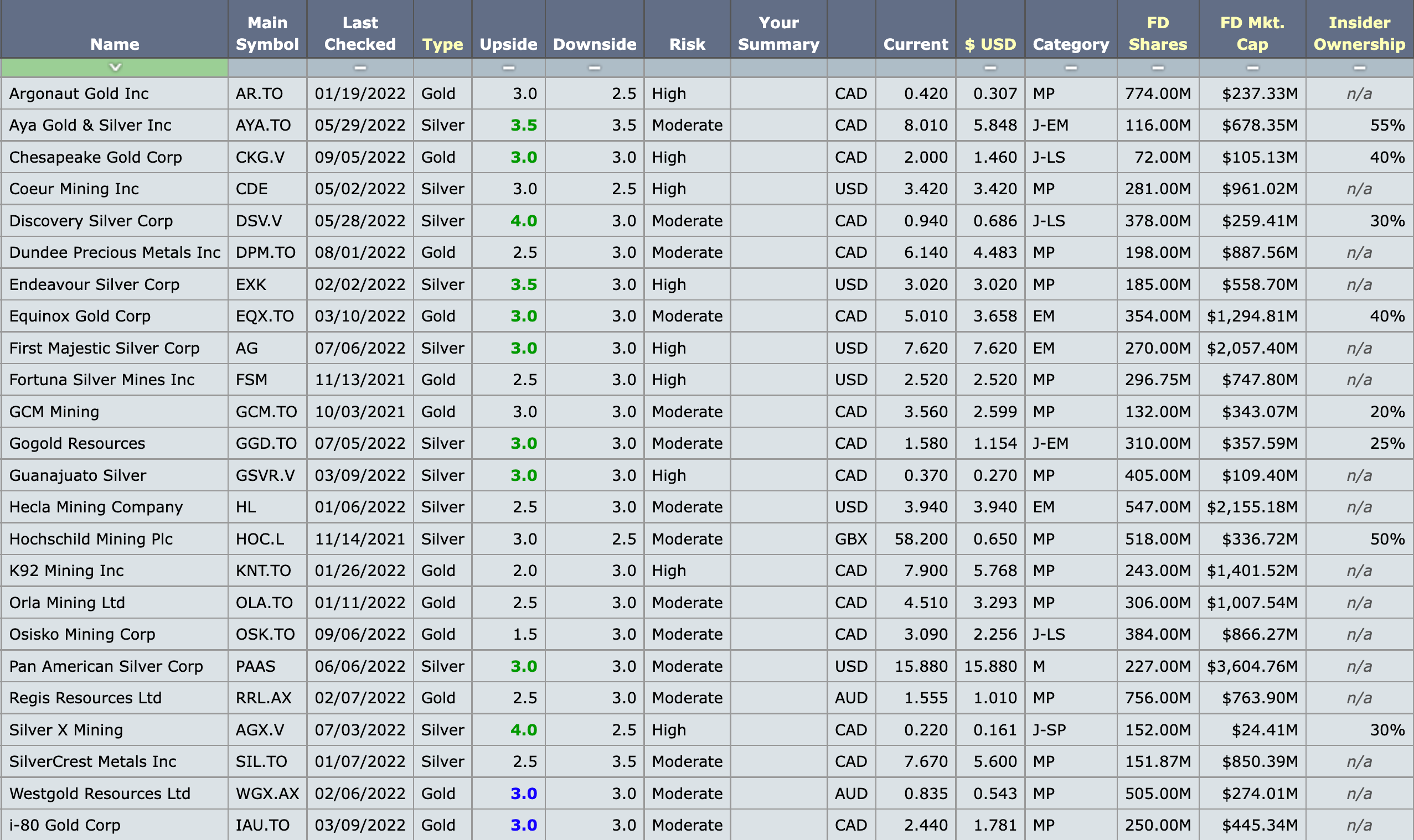

Best of the Best

Favorite Stocks

(Based on $2,500 gold or $100 silver)

My favorite stocks to hold during this bull market. Some of them are moderate risk and others have high risk. Each has its own unique reasons for why I like them.

Changes

Added: Silver X, Equinox, Hochschild, Westgold.

Removed: Gatos (waiting for the resource update).

Top 25 List

(Based on $2,500 gold or $100 silver)

List of the best risk/reward stocks with 5 bagger potential. These are the first stocks I would buy after my foundation of bullion, majors, and mid-tiers was in place.

Changes

Added: Endeavour Silver, US Gold.

Removed: First Mining Gold, Golden Minerals (moved both to 5 bagger list).

1 Bagger List

(Based on $2,500 gold or $100 silver)

List of high quality producers and royalty stocks. Some of them have high risk, but they all have quality management teams and quality properties. Most are good dividend stocks.

Changes

Added: Greatland Gold

Removed:

2 Bagger List

(Based on $2,500 gold or $100 silver)

List of quality stocks with moderate expected returns. These are mostly producers or near-term producers, with a few development stocks.

Changes

Added: Sandstorm Gold, Alkane Resources.

Removed:

3 Bagger List

(Based on $2,500 gold or $100 silver)

List of quality stocks with moderate expected returns. These are mostly producers or near-term producers, with a few development stocks.

Changes

Added: G Mining Ventures.

Removed:

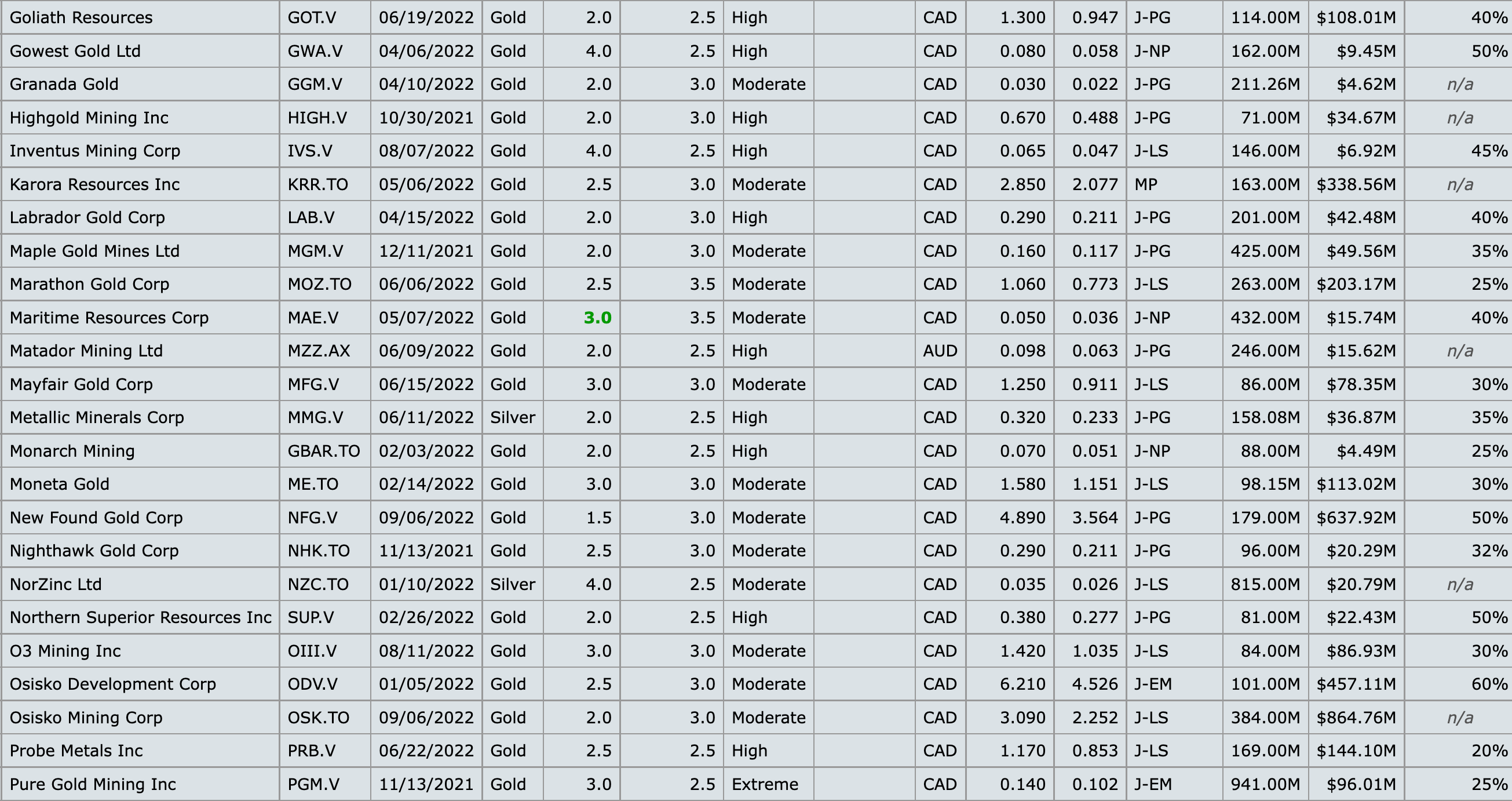

5 Bagger List

(Based on $2,500 gold or $100 silver)

Those in blue are top picks.

Changes

Added: Galiano Gold, First Mining Gold, Golden Minerals.

Removed: Banyan Gold (moved to advanced exploration and optionality exploration).

10 Bagger List

(Based on $2,500 gold or $100 silver)

Those in blue are top picks. All of these stocks can be considered high-risk speculation plays (there is always a reason they are cheap).

See Next Page:

Changes

Added: Apollo Silver, Caracal Gold, Los Cerros.

Removed: Galiano Gold (moved to 5 bagger list). Great Panther (BK), Matador Mining.

Optionality (Exploration)

(Based on $2,500 gold or $100 silver)

List of exploration stocks that have significant resources.

Changes

Added: Banyan Gold.

Removed: Silver Tiger (moved to Optionality Development), Western Copper & Gold.

Optionality (Development)

(Based on $2,500 gold or $100 silver)

List of development stocks that have significant resources.

Changes

Added: Revival Gold, US Gold, Silver Tiger.

Removed: Banyan Gold (moved to Optionality Exploration).

Project Generators - Advanced Exploration

List of project generators who have at least one significant discovery that is being advanced.

See Next Page:

Changes

Added: Banyan Gold, Snowline Gold, Alien Metals, Goliath Resources, Nevada King, Northern Superior, Aztec Minerals, Western Alaska Minerals.

Removed: US Gold (moved to Top 25 and Optionality Developers).

Project Generators - Early Exploration

List of project generators without any significant discoveries. I consider these lottery picks, because they are dependent on finding a discovery.

Changes

Added:

Removed: Snowline, Alien Metals, Goliath Resources, Nevada King, Northern Superior, Aztec (all moved to advanced exploration).

Royalty

List of royalty stocks.

Changes

Added:

Removed: Nomad Royalty (acquired by Sandstorm).

Top Canadian Stocks

Stocks based in Canada or Australia, and mine mostly in Canada.

See next page.

Changes

Added: Goliath Resources, Thesis Gold.

Removed:

Top Australia Stocks

Stocks based in Australia or Canada, and mine mostly in Australia.

See next page.

Changes

Added: Thomson Resources, Alkane Resources, Genesis Minerals, Karora Resources, Tribune Resources, Southern Cross Gold.

Removed: Wiluna (appears to be bankrupt).

Top Silver Stocks

List of Silver Stocks.

See next page.

Changes

Added: Western Alaska Minerals.

Removed: Norzinc (acquired by a private company).

Top Picks Analyzed This Month

1) Goldshore Resources (Late Stage Development): Top 25 List. 4/3 Rating. They are advancing a large open pit project in Ontario. Incredibly, it is down 70% during this current sell-off, and its FD market cap is down to $24M. It’s crazy cheap. At some point, I don’t see how this doesn’t jump to $200M to $300M if gold goes to $2500. Wesdome Gold owns 27% and is not going to give this away for peanuts.

2) Ausgold Ltd (Late Stage Development): 5 Bagger List. 3/3 Rating. They have a large gold project in Australia. They are working on a feasibility to produce 100,000 oz (1 gpt) a year with cash costs around $800 per oz. The project looks pretty solid with a capex under $200M. Plus, it is a large property with a lot of drill targets. They look like they will become another Aussie mid-tier producer.

Stocks Analyzed This Month

Sihayo Gold (Advancing a gold project in Indonesia. 2.5/2.5 Rating. Gold. Late Stage Development. Indonesia).

Freegold Ventures (Advancing a large gold project in Alaska. 2/3 Rating. Gold. Project Generator. USA (Alaska)).

Red 5 Ltd (Gold producer in Australia. 2/3 Rating. Gold. Mid-Tier Producer. Australia).

Silver Tiger Resources (Advancing a large silver/gold project in Mexico. 2/3 Rating. Silver. Project Generator. Mexico).

ATAC Resources (Advancing multiple gold projects in Canada. 2/3 Rating. Gold. Project Generator. Canada (Yukon)).

Galiano Gold (Gold producer in West Africa. 3/2.5 Rating. Gold. Mid-Tier Producer. West Africa (Ghana)).

Lion One Metals (Advancing a gold project in Fiji. 2.5/3 Rating. Gold. Near Term Producer. Fiji).

Chesapeake Gold (Advancing a large gold/silver project in Mexico. 3/3 Rating. Gold. Late Stage Development. Mexico).

Bunker Hill Mining (Advancing a large silver/zinc project in Idaho. 4/2.5 Rating. Silver. Near-Term Producer. Idaho).

Osisko Mining (Advancing a large gold project in Canada. 1.5/3 Rating. Gold. Late Stage Development. Canada (Ontario)).

New Found Gold (Drilling a large gold project in Canada. 1.5/3 Rating. Gold. Project Generator. Canada (Newfoundland)).

G2 Goldfields (Drilling a large gold project in South America. 2/3 Rating. Gold. Project Generator. South America (Guyana)).

Gold Road Resources (Gold producer in Australia. 1.5/3 Rating. Gold. Mid-Tier Producer. Australia).

Northern Star Resources (Large gold producer in Australia and Alaska. 1.5/3 Rating. Gold. Major. Australia, USA (Alaska)).

Thomson Resources (Advancing a silver/gold project in Australia. 3/2.5 Rating. Silver. Late Stage Development. Australia).

Collective Mining (Drilling a large gold project in Colombia. 2/2.5 Rating. Gold. Project Generator. Colombia).

Goldshore Resources (Advancing a large gold project in Canada. 4/3 Rating. Gold. Late Stage Development. Canada (Ontario)).

Asante Gold (Gold producer in West Africa. 2/2.5 Rating. Gold. Mid-Tier Producer. West Africa (Ghana)).

Tempest Minerals (Drilling several gold projects in Australia. 2/2.5 Rating. Gold. Project Generator. Australia).

Altiplano Metals (Small copper/gold producer in Chile. 2/2.5 Rating. Gold. Small Producer. Chile, Nicaragua).

New Pacific Metals (Advancing a large silver project in Bolivia. 2.5/3 Rating. Silver. Late Stage Development. Bolivia, Canada (Yukon)).

Apollo Silver (Advancing a large low-grade silver project in California. 4/2.5 Rating. Silver. Late Stage Development. USA (California)).

Velocity Minerals (Advancing a small gold project in Bulgaria. 3/2.5 Rating. Gold. Late Stage Development. Bulgaria).

Platina Resources (Drilling several gold projects in Australia. 2/2.5 Rating. Gold. Project Generator. Australia).

Catalyst Metals (Small gold producer and drilling several projects in Australia. 2.5/3 Rating. Gold. Small Producer. Australia).

Caracal Gold (Small gold producer in East Africa. 4/2.5 Rating. Gold. Small Producer. East Africa (Kenya, Tanzania)).

Banyan Gold (Drilling a large gold project in Canada. 2/3 Rating. Gold. Project Generator. Canada (Yukon)).

Alkane Resources (Gold producer in Australia with large low-grade deposit. 2.5/3 Rating. Gold. Emerging Mid-Tier Producer. Australia).

Arizona Silver Exploration (Drilling a gold project in Arizona. 2/2.5 Rating. Gold. Project Generator. USA (Arizona)).

Manuka Resources (Small gold producer and a low-grade silver project in Australia. 2.5/2.5 Rating. Silver. Small Producer. Australia).

Blue Lagoon Resources (Advancing a small gold project in Canada. 2/2.5 Rating. Gold. Near-Term Producer. Canada (British Columbia)).

Los Cerros (Advancing a gold project in Colombia. 4/2.5 Rating. Gold. Late Stage Development. Colombia).

Nexus Minerals (Advancing a gold project in Australia. 2/2.5 Rating. Gold. Project Generator. Australia).

Genesis Minerals (Advancing a gold project in Australia and trying to acquire Dacian Gold. 2/2.5 Rating. Gold. Late Stage Development. Australia).

West Wits Mining (Advancing a gold project in South Africa. 4/2 Rating. Gold. Late Stage Development. South Africa, Australia).

Norsemont Mining (Advancing a gold project in Chile. 2/2 Rating. Gold. Late Stage Development. Chile).

Ausgold Ltd (Advancing a gold project in Australia. 3/3 Rating. Gold. Late Stage Development. Australia).

Japan Gold (Drilling a gold project in Japan. 2/2.5 Rating. Gold. Project Generator. Japan).

RTG Mining (Advancing a small gold project in the Philippines. 2.5/2.5 Rating. Gold. Late Stage Development. Philippines, PNG, Kyrgyz Republic).

Carnaby Resources (Drilling a copper/gold project in Australia. 2/2.5 Rating. Gold. Project Generator. Australia).

Lara Exploration (Drilling base metals and gold projects in Brazil and Peru. 2/2.5 Rating. Gold. Project Generator. Brazil, Peru).

Gold Terra (Advancing a gold project in Canada. 4/2.5 Rating. Gold. Late Stage Development. Canada (NWT)).

Navarre Minerals (Small gold producer and explorer in Australia. 2/2.5 Rating. Gold. Small Producer. Australia).

Capitan Mining (Drilling a silver project in Mexico. 2/2.5 Rating. Silver. Project Generator. Mexico).

Pan African Resources (Gold producer in South Africa. 1.5/2.5 Rating. Gold. Mid-Tier Producer. South Africa).

China Gold Intl (Gold producer in China. 1.5/2.5 Rating. Gold. Mid-Tier Producer. China).

Vast Resources (Small copper/gold producer in Romania. 2/2.5 Rating. Gold. Small Producer. Romania).

Rover Metals (Drilling a gold project in Canada. 2/2.5 Rating. Gold. Project Generator. Canada (NWT)).

Investment Bias

I want to clarify how I do my ratings and the focus of my valuations. My investment bias is on future cash flow at $2500 gold and $100 silver. For this reason, I put very little emphasis on the short-term. My ratings are future based (3-5 years). Moreover, if I am wrong about gold reaching $2500 in the next 3-5 years, then my ratings likely will fall short. Thus, by using a future bias I am introducing a high level of risk.

The Top 25 are the best risk/reward stocks at $2500 gold and $100 silver. The Top Picks include stocks that I consider 5+ baggers at $2500 gold and $100 silver, have 3 ratings or higher, and do not have any significant red flags. Significant red flags would include high debt, low cash, financing issues, location issues, growth issues, legal issues, timeline issues, management issues, etc.

Disclaimer

The information contained in the newsletter has been obtained from sources believed to be reliable, but there is no guarantee as to the completeness or accuracy and it should be validated by yourself. There may be factual errors. Because individual investment objectives vary, information on this website should not be construed as advice to meet the particular needs of the reader. Don Durrett et al. are not financial advisors and none of this information should be construed as financial advice. Any opinions expressed herein are statements of our judgment as of this date and are subject to change without notice. Any action taken as a result of reading this independent market research is solely the responsibility of the reader. Don Durrett et al. are not and do not profess to be professional investment advisors, and strongly encourage all readers to consult with their own personal financial advisors, attorneys, and accountants before making any investment decision. Don Durrett et al. and/or independent consultants or members of their families may have a position in the securities mentioned. Investing and speculation are inherently risky and should not be undertaken without professional advice. Always do your own due diligence before making an investment decision. Understand that mining stocks are high risk investments, situations change rapidly and there is considerable risk on many fronts: political, legal, operational, market and environmental. Following and/or acting on any information blindly and without personal justification is foolhardy and likely to result in a bad outcome. By your act of reading this website, you fully and explicitly agree that Don Durrett et al. will not be held liable or responsible for any decisions you make regarding any information discussed herein.

When is Novembers newsletter?

Well done don